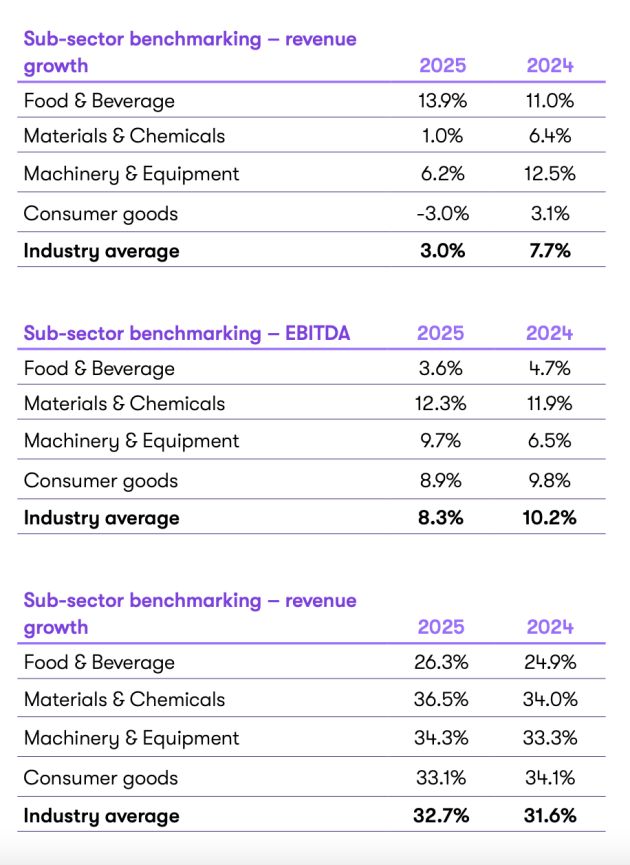

One of the world’s largest accounting firms, Grant Thornton, has released its 2025 Manufacturing Benchmarking report, examining the financial data of 100 mid-sized Australian manufacturers. The food and beverage sector continues to stand out, leading in revenue growth across the wider industry.

Like most businesses across Australia, mid-sized manufacturers are in the midst of a cost-conscious and complex environment, navigating through supply chain constraints, cost pressures and global competition.

The latest data from Grant Thornton shows a story of innovation and adaption in the face of these challenges, with a group of top performers growing revenue more than six times faster than average, freeing up capital and allowing them to invest in automation, product innovation, and digital infrastructure.

The top manufacturers have continued to deliver strong results with 18 per cent sales growth, compared to the industry average of 3 per cent this year. In contrast to the wider industry, stronger performing manufacturers appear to be retaining more earnings.

However, while there’s growth in the sector for those focused on strategic priorities, it’s clear there is an overall softening in the sector reflective of a broader economic slowdown.

Manufacturers with revenue above $75 million have increased gross profit percentage from 31 per cent to 33 per cent, mirroring the top performer results, while businesses below $75 million experienced a sharp contraction in gross margin – from 36.2 per cent to 32.6 per cent.

EBITDA multiples have decreased to 8.3x, marking the manufacturing industry's second consecutive year of decline in EBITDA margins – now below those seen in 2022 – likely due to ongoing inflationary pressures impacting costs. Notably, EBITDA improved for businesses with revenue under $75 million, indicating strong cost management during the year, particularly given a decreased gross margin.

Grant Thornton national head of manufacturing, Michael Climpson, said the analysis showed that success in the industry hinges on the ability to manage cost pressures and complexity while continuing to invest in capability, innovation and technology.

“The current economic slowdown provides an opportunity to re-evaluate future strategies,” said Climpson.

“This could involve securing government grants for investments in technology and innovation, exploring new product lines and markets, or leveraging mergers and acquisitions to enhance scale and diversify operations.”

Source: Grant Thornton

Food and beverage sector

The food and beverage sector leads in revenue growth, outperforming the industry average by almost 11 per cent, achieving 13.9 per cent compared to the overall manufacturing average of 3.0 per cent.

The data indicates businesses positioned around health, sustainability, and innovation are capturing more market share and driving the food and beverage sector’s overall growth.

Climpson reiterated this, telling Food & Drink Business that growth is largely being driven by rising consumer demand for health-conscious, locally sourced and sustainable products.

“However, the subsector’s average EBITDA margin was significantly lower than peers at 3.6 per cent – a result influenced by a small number of companies experiencing significant losses,” said Climpson.

“When these large-loss outliers are excluded, the average EBITDA margin lifts to 14 per cent, outperforming the rest of the sector. This reflects stronger profitability across the broader cohort, particularly for businesses with established supply chains and scalable operations.”

The report also observed the disparity in EBITDA margin largely reflects the presence of many entrants striving to keep up with trends in consumer preferences. In contrast, well-established brands manufacturing more staple products continue to have greater control over price and cost management.

Climpson also noted the company’s data suggests that food and beverage manufacturers have continued to invest in production capability, with CAPEX sitting around 8 per cent of revenue – well above the industry average.

“While this figure is partially skewed by one outlier’s significant investment in land and buildings, the overall trend reflects ongoing investment in innovation and efficiency,” said Climpson.

“These investments are particularly important for subsectors like food and beverage manufacturing, where efficiency and responsiveness to consumer trends are critical.”